By Cristian Gallorini[1]

Legal stability and predictability are core elements of the rule of law. In the case of foreign investments in renewable energy (RE) the concept of stability imbues distinct aspects of the investment cycle, including the arbitrability of disputes. First, stability of the investment conditions is fundamental to foreign investors. Second, International Investment Agreements (including the Energy Charter Treaty, ECT) and investment standards generally entail an element of stability. Last, as noted by Wöss, stability is also at the core of the role and function of compensation of damages which is to provide “stability in legal relationships and prevents opportunistic behavior.”

The next paragraphs focus on the element of stability as encompassed by the Fair and Equitable Treatment standard (FET). I first argue that the FET entails an element of stability as an obligation independent of the obligation to respect legitimate expectations. I then address that a viable method to analyze a breach of the obligation of stability under the FET is the proportionality analysis used by the constitutional courts and the Court of Justice of the European Union (CJEU). I bring Blusun v. Italy, as an example of the codification of the proportionality analysis, and Eurus v. Spain as an example for its application. I conclude that both an obligation of stability and proportionality analysis are finding recognition as independent concepts in international investment law and public international law, shifting the tribunals’ analysis of the FET from an analysis primarily centered on the investor’s legitimate expectations to an analysis in which legitimate expectations are mere consideranda.

The Element of Stability in the FET. Obligation to Stability or Obligation to Respect Legitimate Expectation of Stability?

The FET is the most invoked provision in investment treaty arbitration. Yet the vagueness of the FET raises several interpretative problems where, for example, arbitral tribunals must assess a breach of the FET because of the host state adoption of legislation that affects investments made under prior regimes. In these types of cases, the FET standard entails a certain element of stability of the regulatory framework that is compromised in “situation[s] where the law [keeps] changing continuously and endlessly, as [does] its interpretation and implementation” (PSEG, Award, para 254).

Assessing a breach of the FET under the element of stability requires an analysis of the measures implemented in the exercise of the states’ sovereign power to legislate weighted against the interests of the investors. Arbitral tribunals have addressed the issue in two fashions. Most tribunals have applied a balancing test determining the right balance between the state’s sovereign power to legislate and amend the regulatory framework, on one hand, and the investor’s legitimate expectation on the other. According to this interpretative approach, investors would have a legitimate expectation of stability created by the regulatory framework existing at the time of the investment. If the new regulatory framework unnecessarily, or disproportionately frustrates the investor’s reasonable and legitimate expectations, then there is a breach of the FET. Less often, arbitral tribunals have analyzed the state’s obligation to maintain a stable legal framework as part of the FET independently of any consideration of legitimate expectations. In these cases, importance is given to whether the regulatory changes are necessary and proportionate to the aim of the legislative amendment. The investor’s legitimate reliance becomes only one of the factors that may be considered in the tribunal analysis, but it is not the primary element in which the analysis is based on. The latter approach, like the former, does not presuppose that a regulatory framework will never be changed. But it implies that a change of the regulatory framework that is radical, abrupt, fundamental, unnecessary, or unsuitable to achieve the objective it pursues, will violate the FET – without the need of an assessment of the investor’s reliance on the earlier regime.

Furthermore, as noted by Maynard, the starting point in both the interpretative approaches is the same: a tribunal “will objectively consider the particular circumstances of the State and what could reasonably have been expected of it in light of those circumstances”. Moreover, no host state’s deliberate intention of bad faith in adopting the measures is an essential element of the FET even though its existence could aggravate the situation. Yet a breach of legitimate expectations of (stability), would “requires a tribunal to [additionally] consider whether, subjectively, an investor actually held that expectation and, objectively, whether it was reasonable for it to do so.”

Thus, an interpretation of the element of stability as applied to FET requires first an answer to whether the principle of stability exists as a standalone, legally distinct obligation in international investment law or public international law. I argue that it does, as a series of investor-state decisions and awards based on a first generation of BITs and the ECT show.

The Obligation of Stability in the first generation of BITs and interpretation of Article 10(1) ECT

The idea of an obligation of stability as a distinct element of the FET has been recognized at least since the early 2000s. In a first line of investor-state arbitrations, tribunals have affirmed that “stability of the legal and business framework is . . . an essential element of [FET]” (Occidental Exploration & Production Company, Award, para. 183; see also CMS, Award, para. 274). Notably, in these cases – all based on BITs to which the United States is a party – the applicable BITs did not include any definition of the FET. Instead, the tribunal could support the existence of an obligation of stability by reference to the BITs’ preambular language expressing the idea that “fair and equitable treatment of investment is desirable in order to maintain a stable framework for investment.” (See, e.g., 1993 Ecuador-United States BIT, 1991 Argentina-United States BIT).

More recently, a distinct element of stability seems to have found recognition in the interpretation of Article 10(1) ECT, in the context of subsidies or special benefits for the RE sector. In Blusun, the Tribunal noted that the requirements to “encourage and create a stable, equitable . . . conditions for [foreign investors]” of Art. 10(1) ECT, 1st sentence, is distinct obligation from the one “accord[ing] at all times to [i]nvestment of [foreign investors] fair and equitable treatment” (Blusun, Award, para. 363). On this consideration the Blusun Tribunal divided its analysis into breach of legal stability on the one hand, and breach of the FET under the lenses of the obligation of respect investor’s legitimate expectations, on the other. In Charenne, the Tribunal affirmed that the “obligation to provide fair and equitable treatment is included in the more general obligation to create stable, equitable, favourable and transparent conditions” of Article 10(1) ECT, 1st sentence (Charenne, Award, para. 477). Similarly, for the Novenergia II Tribunals, the FET embraces an “obligation to provide fundamental stability.” (Novenergia II, Award, para 645). Yet for the Novenergia II Tribunal the obligation of stability is not a standalone obligation but “simply an illustration of the obligation to respect the investor’s legitimate expectations through the FET” (Novenergia II, Award, para. 646). There, the “primary element” of the FET remains the “legitimate and reasonable expectations of the Claimant” and its most important function is its protection (Novenergia II, Award, para. 646). And the assessment of whether the FET has been breached takes the form of a “balancing exercise where the state’s regulatory interests are weighed against the investor’s legitimate expectations and [reasonable] reliance” on those expectations (Novenergia II, Award, para. 694).

Most of the Spanish Renewable Saga cases applies a version of the balancing test used in Novenergia II, and, with different outcomes, the element of stability happens to be just another factor in the analysis of the investor’s legitimate expectations. At the same time, in Eurus (and its twin decision BayWa) the analysis is inverted. There, centrality is given to the obligation of stability, and the investor’s legitimate expectation becomes only a consideranda in the analysis of whether the host state’s measures are proportionate to their legislative aims (Eurus, Decision para. 317). Eurus is thus distinguishable from other cases involving the Spanish renewable energy reform because it recognizes the existence of a principle of stability in Article 10(1) of the ECT, distinct from the existence (and breach of) the investor’s legitimate expectations. And the legitimate expectations are no more than a factor to be factored in the analysis of a breach of the FET (Eurus, Decision para 355).

In sums, an obligation of stability as a distinct element of the FET seems to find recognition as a principle of international customary law as interpreted in first generation of BITs – buttressed by the preamble of the applicable BITs – as well as in the interpretation of Article 10(1) ECT – buttressed by its first sentence. It remains to analyze what is the correct test to be applied to analyze a breach of the FET under its element of stability. I argue that the correct test is a version of the proportionality test as codified in a dictum by the Tribunal in Blusun.

The Blusun test as an application of the Proportionality analysis to breaches of the obligations of stability

Since the earliest stages of investor-state arbitration discussed above, the finding of a breach of stability under the FET has been considered a high standard. The existence of an obligation of stability never implied that the regulatory framework would remain unchanged for the entire life of an investment. It has instead required the measures to amount to “a total alteration of the entire legal setup for foreign investments” (El Paso, Award, para. 517) or a “[complete dismantlement] of the very legal framework constructed to attract investors” (LG&E, Decision on Liability, para. 139).

But how can a breach of stability as a distinct element of the FET be assessed in concrete terms? Arguably, a proportionality analysis, like that applied by constitutional courts after World Word II, or the Court of justice of the European Union to review EU law and national measures, seems to be a viable answer. Traditionally, the proportionality analysis has been construed as a three-prong test. First, (1) the disputed measures must be suitable or appropriate to achieve the objective they pursue (suitability); second, (2) no other alternative measure should exist that is less restrictive and equally effective in achieving the objective (necessity); and finally (3) the disputed measures should not be disproportionate were weighed against the other interests involved (proportionality stricto sensu). Yet courts and tribunals do not always apply the three-prong test as such: sometimes they may even disregard some of the elements. This is the case, for example, of the necessity prong which is most often left to the legislator to determine. At times, the entire proportionality analysis, as noted by Marzal, is reduced to “as substantially equivalent to balancing.”

In the context of investor-state arbitration in the RE under the ECT, Marzal’s statement acquires significance when juxtaposed to the primary relevance that investor’s legitimate expectations have in the analysis of a breach of Article 10(1), 1st and 2nd sentence of the ECT. In most of the Spanish renewable saga cases, an analysis of an alleged breach of Article 10(1) ECT is indeed generally determined under the lenses of the balancing test weighing the state’s sovereign power to legislate and amend the regulatory framework against the investor’s legitimate expectations. Limited space is given in that analysis to the suitability or the necessity prongs. That said, other arbitral tribunals seem to have, more or less explicitly, codified the proportionality analysis in their analysis of breach of Article 10(1) ECT. Blusun v. Italy is a good example of it. Blusun concerned regulatory changes in the Italian energy sector reform and judicial measures that, according to the investor, had the claimed effect to frustrate its investment in a 120 MW power solar project in the Region of Puglia. There, in a dictum the Tribunal created an interpretative roadmap to assess a breach of Article 10(1) ECT that retraces the classical proportionality analysis. The test reads as follows:

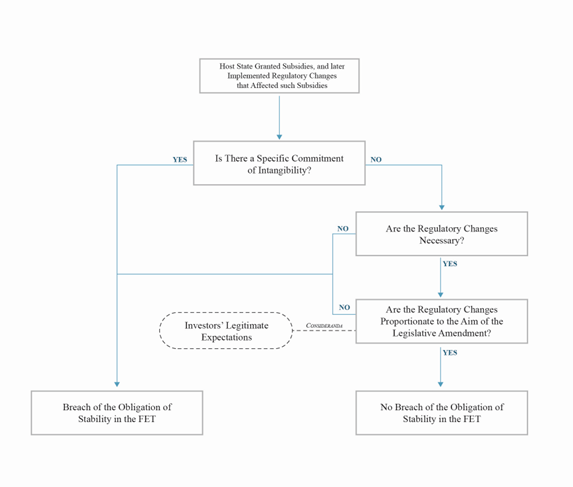

In the absence of a specific commitment, the state has no obligation to grant subsidies such as feed-in tariffs, or to maintain them unchanged once granted. But if they are lawfully granted, and if it becomes necessary to modify them, this should be done in a manner which is not disproportionate to the aim of the legislative amendment, and should have due regard to the reasonable reliance interests of recipients who may have committed substantial resources on the basis of the earlier regime.

(Blusun, Award para. 319(5) emphasis added).

The Blusun test is based on three premises. First, the existence of a general regulatory framework granting subsidies or special benefits for foreign investors to attract investment. General regulatory framework usually consists of law, policies and regulations of general application that existed at the time of the investment and played a significant role in the investors’ decision to invest. Second, subsequent regulatory changes that affect such subsidies or special benefits. Third, the absence of an implicit or explicit undertaking by the host state—a specific commitment the breach of which would breach Article 10(1) ECT. According to the Blusun Tribunal, in the absence of a specific commitment, identifying a breach of the FET would therefore require an analysis of whether the regulatory changes are necessary and proportionate to the aim of the regulatory change (first two prongs of the proportionality test), with due regards to the reasonable reliance interest of the investors (proportionality stricto sensu).

An application of the Blusun dictum in the terms presented here, is found in Eurus v. Spain, which is one of the Spanish Renewable saga cases. Eurus involved the Japanese Eurus Energy Holdings Corporation investment made in 13 wind farms in Spain between 1997 and 2006 (with one commissioned later in 2008) and motivated by Spain regulatory regime that entitled investor in the RE to receive special remunerations. Starting from 2007, however, Spain implemented a series of regulatory changes, and measures that overhauled the special regime and ignited the about fifty-six investor-state arbitration against Spain. In 2013, as part of these regulatory changes, Spain eliminated the special regime and introduced measures that took into account the earlier subsidies to assess future payments. These measures ended up reducing payments of subsidies “that would have otherwise been made by reference of payments lawfully made in the past in respect of past production,” the so-called claw-back feature of the disputed measures (Eurus, Decision, para. 349). Analyzing the claw-back feature of the disputed measures, the Eurus Tribunal held that by implementing regulatory changes that retroactively clawed back subsidies duly paid to the investor based on prior regulatory regime, Spain breached the principle of stability in Article 10(1) ECT. And because of Spain’s breach, the Tribunal awarded Eurus $106 million.

Setting aside the conclusion reached by the Tribunal, what is relevant here is the way the Tribunal assessed the breach of Article 10(1) ECT. First, the Tribunal relied on the Blusun dictum as roadmap for its analysis (Eurus, Decision para. 315). Second, the Tribunal affirmed that legitimate expectations are only consideranda, and “there is no rule that legitimate expectations are to be observed” (Eurus, Decision para. 317). According to the Tribunal “there was no acquired right to remuneration in the future, still less to a fixed and unchanging FIT.” The claw-back issue was not about whether there was an expectation that the subsidy would not have changed for the future, but whether future subsidies, that would have otherwise been made, could be reduced by reference to payments lawfully made in the past in respect of past production (Eurus, Decision para. 349). Third, the Tribunal identified the existence of an “obligation of stability,” that Spain breached “by eliminating future subsidies otherwise payable by reference to amounts lawfully paid” under the earlier regulatory regime (Eurus, Decision para. 354). The Tribunal thus concluded that (i) “no contractual right or legitimate expectation to an unchanging subsidy in any form” exists; and (ii) the claw back feature of the disputed measure breached the FET because the claw back feature is “inconsistent with the principle of stability in Article 10(1) of the ECT” and unnecessary to resolve the tariff deficit problem (Eurus, Decision para. 355).

The Eurus Tribunal analysis is nothing more than the application of the proportionality analysis to a breach of Article 10(1) ECT. In other words, the Tribunal reasoned that although the disputed measures may have been suitable to solve the Spanish tariff deficit problem, the claw back feature of the disputed measures was not necessary to resolve the tariff deficit (the less restrictive disputed measures without the claw-back features would have equally solved the problem). Because the claw-back feature did not pass the necessity prong of the proportionality analysis, there was no reason for the Tribunal to account for the investor’s legitimate expectations (proportionality stricto sensu).

To conclude, Eurus shows that the Blusun dictum offers a viable tool for an analysis of breach of the distinct obligation of stability in the FET. However, someone could argue, as Garibaldi did in Eurus dissenting opinion, that the Blusun test is an arbitrator-made test that does not necessarily coincide with an application of the FET (Eurus, Dissenting Opinion, para. 30). Nonetheless, the Blusun dictum seems to provide a well-suited roadmap for the analysis of possible breaches of the FET as a consequence of alteration or dismantlement of regulatory frameworks in the RE sector.

The Obligation of Stability and the Proportionality Analysis are Finding Recognition as Independent Concept in International Investment law and Public International law

As a result of the analysis that precedes, it seems that both an obligation of stability and the proportionality analysis are finding recognition as independent concepts in international investment law and public international law. Eurus v. Spain is one of the most recent examples of this proposition in the analysis of breaches of Article 10(1) ECT. Moreover, the tribunals’ analysis of a breach of the obligation of stability in the FET may be slowly shifting from an analysis of the FET primarily centered on the investor’s legitimate expectation to an analysis in which legitimate expectations are mere consideranda. Yet, this is still a minority view. A tentative reason for a limited applicability of this approach may be found in the argument that an analysis that centers excessively on the proportionality of a regulatory framework may be assimilated to a legality review, and, if brought to an extreme, may fall beyond the scope of the tribunals’ jurisdiction. To conclude, it remains to be seen how arbitral tribunals will address the breach of stability in the FET in the near future and whether the minority approach will eventually gain more relevance.

-

Cristian Gallorini is a New York Attorney at Barakat + Bossa PLLC and Junior Editor of the EFILA Blog. This post is partly based on the research conducted by the author for the presentation of the ICSID Case No. ARB/16/4, Eurus v. Spain delivered with Takashi Yokoyama in front of the JIRDC-Tokyo Study Group on Investment Arbitration Case Studies. The views expressed in this post are solely of the author and do not reflect the views of the organizations the author represents. ↑